How to Afford a 1 Crore Health Insurance Plan: A Smart Strategy

A 1 crore health insurance plan offers comprehensive coverage for significant medical emergencies. However, the premium for such a high sum insured can be substantial. A smart strategy to make it more affordable is to combine a base health insurance policy with a top-up or super top-up policy.

Understanding the Basics

- Base Health Insurance: This is your primary health insurance policy that covers a specific sum insured, usually ranging from 5 to 10 lakhs. It pays for all your medical expenses up to the limit of the sum insured.

- Top-up or Super Top-up Policy: These policies act as an add-on to your base policy. They provide additional coverage over and above the limit of your base policy. They come into effect only after your base policy sum insured is exhausted.

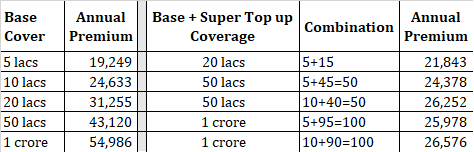

How to Structure Your 1 Crore Health Insurance

- Choose a Base Policy:

- Select a base policy with a sum insured that covers your routine medical expenses. A sum insured of 5 to 10 lakhs is a good starting point for most individuals and families.

- Add a Top-up or Super Top-up Policy:

- To reach the 1 crore coverage, you can opt for a top-up or super top-up policy.

- Top-up Policy: This policy has a specific threshold limit. Once your base policy sum insured is exhausted, the top-up policy starts covering the remaining expenses, up to its limit.

- Super Top-up Policy: This policy has a deductible. Once your medical expenses exceed the deductible, the super top-up policy pays the remaining amount, up to its limit.

Advantages of this Strategy:

- Lower Premiums: By splitting the coverage, you can significantly reduce the overall premium compared to a single 1 crore policy.

- Tax Benefits: Both base and top-up/super top-up policies often qualify for tax benefits under Section 80D of the Income Tax Act.

- Flexibility: You can customize your coverage based on your specific needs and budget.

Important Considerations:

- Waiting Period: Be aware of the waiting periods for certain illnesses and procedures, especially for pre-existing conditions.

- Room Rent Limits: Check the room rent limits imposed by your insurer.

- Network Hospitals: Ensure that your chosen insurers have a wide network of cashless hospitals.

- Claim Process: Understand the claim process and the required documentation.

By combining a base policy with a top-up or super top-up policy, you can achieve comprehensive health insurance coverage at a more affordable premium. Always consult with an insurance advisor to choose the best combination of policies that suit your specific needs and budget.